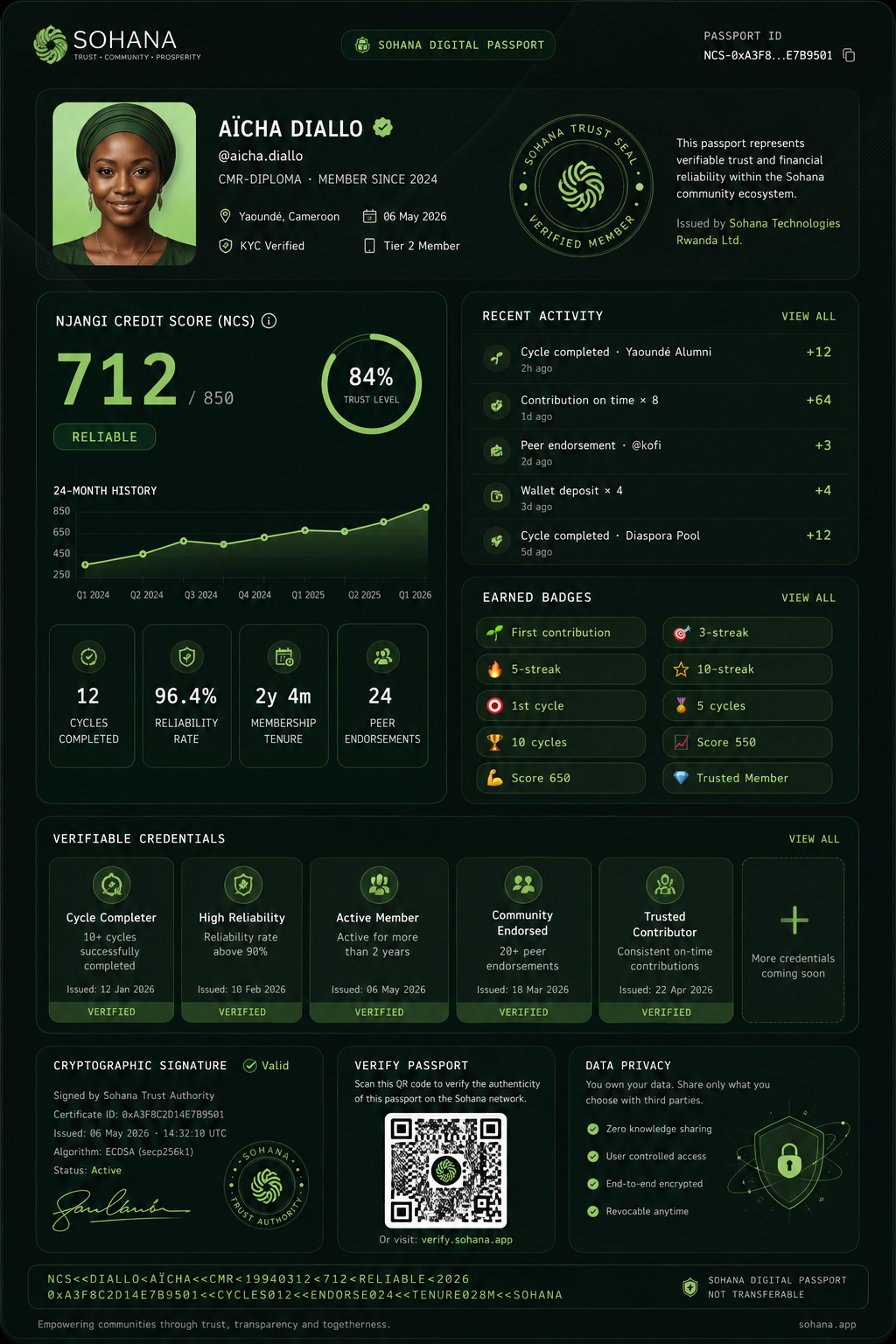

A digital résumé that travels with you.

The Circle Passport is your portable NCS credential — a beautifully designed digital document that summarises your entire Sohana history at a glance. Score. Tier. Years on the platform. Cycles completed. Reliability percentage. Endorsements earned. Badges. Every figure that matters, in one place. Designed to be presented to a landlord, a lender, a partner business, or simply to look at when you want to feel proud of what you have built.

Today the passport lives inside Sohana. As we secure partnerships across the continent, the same passport becomes a credential you can present off-platform — verified cryptographically, owned by you, never sold to anyone. It is the visible artefact of years of trustworthy behaviour.

Generate your Passport now

Members with any completed cycle can generate and download their own Sohana Digital Passport. It updates automatically as your NCS score changes, and you decide when to share it.

- ✓ Download as PDF or PNG

- ✓ Share via QR code or direct link

- ✓ Verifiable by any partner or lender via verify.sohana.app

- ✓ Revocable at any time — you own the data

The passport is yours, owned by you, and never displayed without your active permission. Cryptographic signing and external verification are on the 2027 roadmap for continental partner recognition.